Decoding Attrition and Building Long-Term Value in Microfinance

This blog draws on a well-regarded paper on customer retention in credit products, based on my research across five countries in Latin America and the Caribbean. Although the study was conducted several years ago, its lessons remain highly relevant—especially today, as technology offers new tools to help microfinance institutions (MFIs) overcome the traditional limitations of microcredit.

Many MFIs continue to lose customers because they rely on outdated, sales-driven approaches that prioritize loan disbursement over meeting customer needs. By understanding why clients leave, MFIs can design better products, improve retention, and foster long-term customer relationships.

Why retention matters? Not just because it lowers acquisition costs, but because loyalcustomers fuel future growth and strengthen an institution’s value. Two MFIswith similar financials can have vastly different valuations if one enjoysstronger customer loyalty.

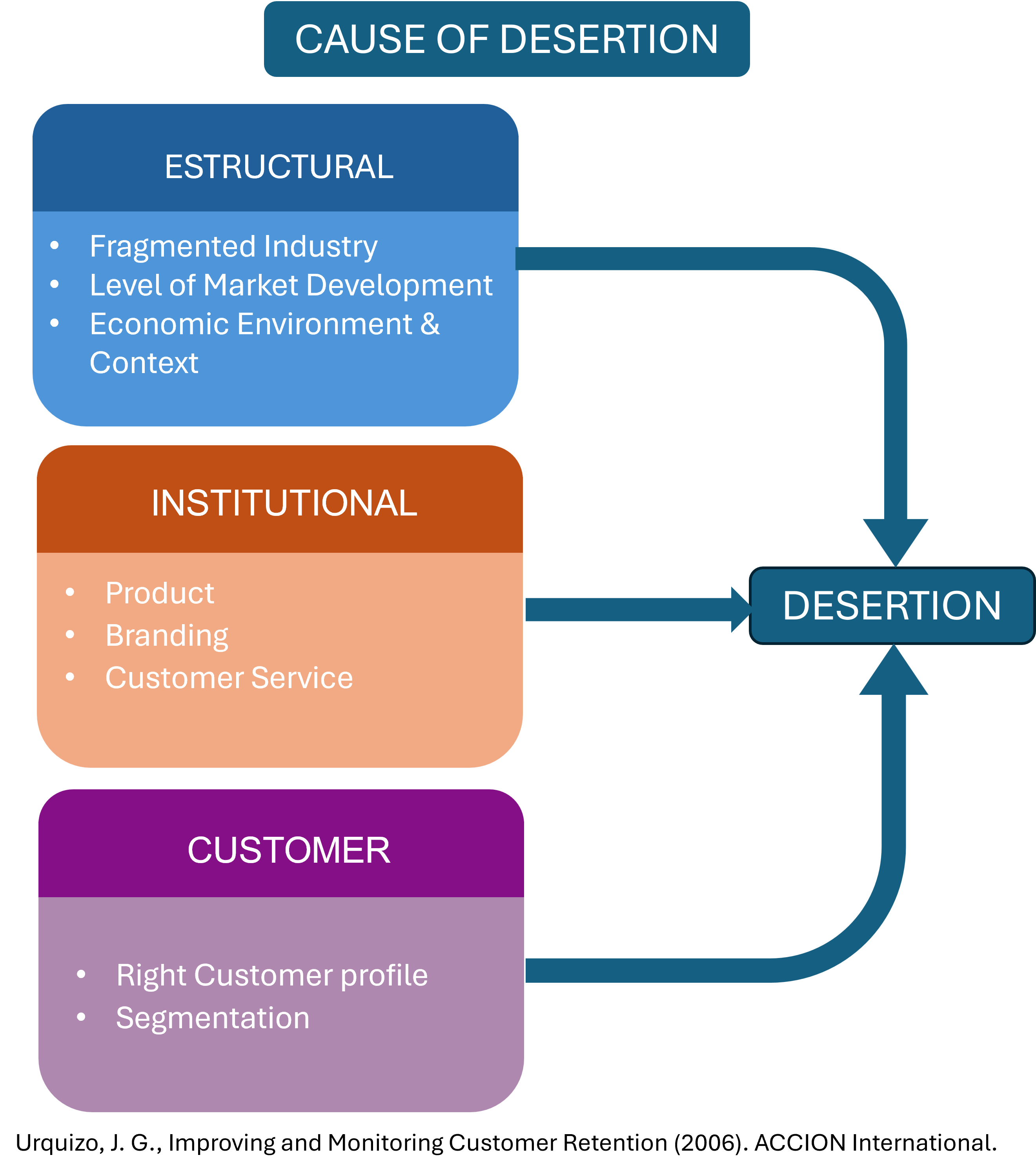

What Drives Client Attrition?

To boost retention, MFIs must first understand why clients leave. Thecauses are varied and interconnected, but we’ll explore them in three dimensions.

1️. Industry Context Factors

A. Market Evolution & IndustryDynamics

- Fragmented markets and low entry barriers fuel intense competition.

- Both large and small MFIs compete locally by offering personalized service—a model that’s hard to scal

- High staff turnover and limited product differentiation drive client churn.

- Competition focused on credit volume can result in over-indebtedness and parallel credit usage.

- Industry consolidation is rare due to mission alignment challenges and weak brand influence—scaling for cost efficiencies remains difficult.

B. Product & Market Maturity

- In mature markets, customers are well-informed and increasingly empowered.

- Good credit clients develop negotiation power, seeking value-added solutions.The traditional microfinance model (small, incremental loans) no longer fits the needs of seasoned entrepreneurs.

- Some MFIs, in pursuit of growth, move into higher-risk segments, whichincreases unsustainable churn.

C. Local Economic Factors

- Regional economic conditions strongly influence borrowing behavior.

- “Resting” clients (temporarily pausing credit use) are a normal response to seasonal cycles—not true deserters.

- Monitoring local business cycles and consumer confidence can help predict demand.

2️. MFI Performance Factors

A. Product Frustration

- Rigid, one-size-fits-all products limit flexibility.

- Lack of differentiation encourages multi-borrowing.

- Clients value loan size and terms even more than interest rates.

- Overly conservative loan officers can drive clients away.

- Rewarding loyal clients is powerful—but challenging under current pricing models.

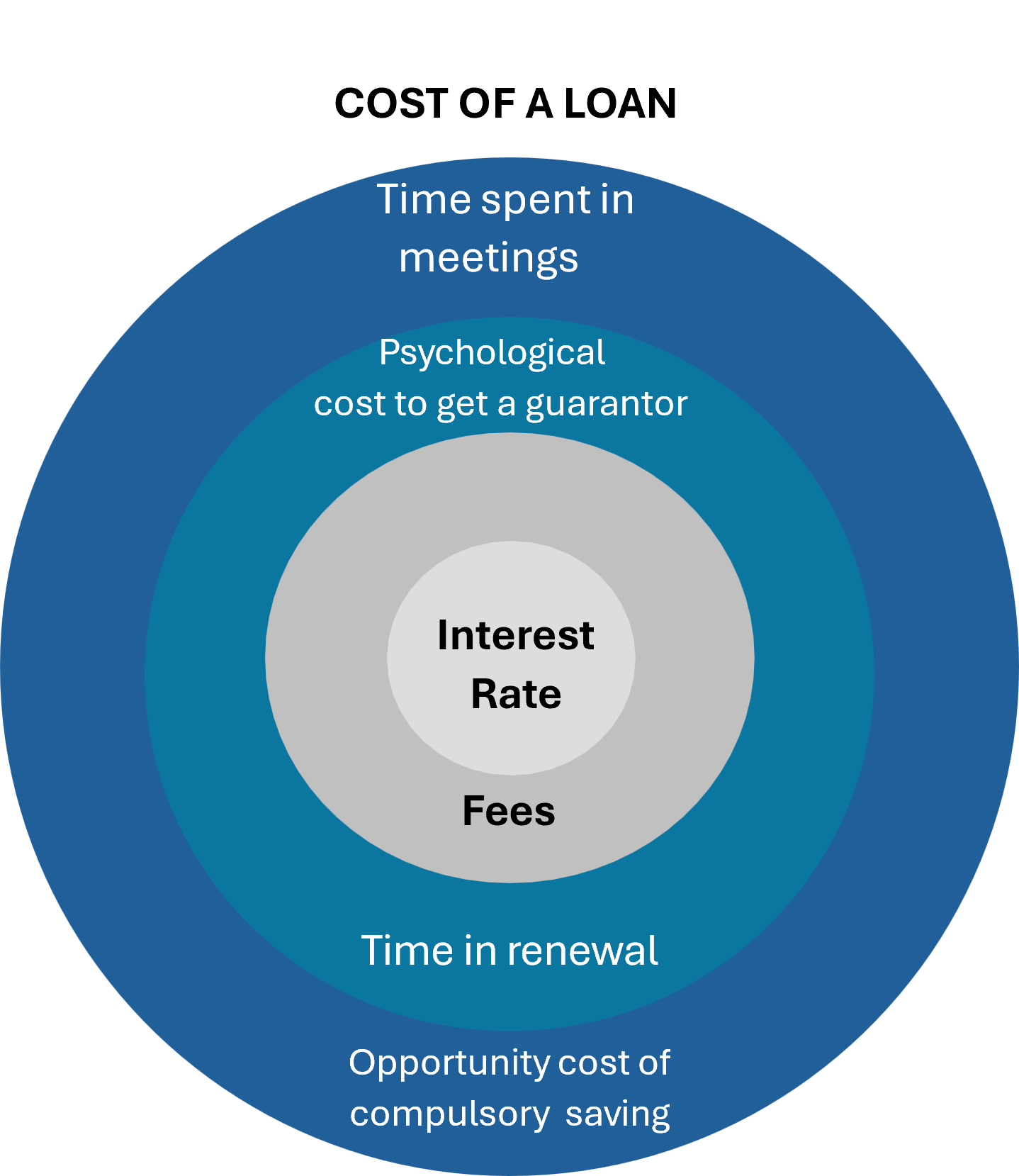

- The total cost of credit is not sustainable for micro-entrepreneurs; in fact, loans can sometimes leave them even poorer.

B. Customer Service

- According to research, poor service drived only 3–10% of attrition.

- Clients often tolerate weak service due to strong relationships with loan officers.

- Significant service improvements require investment—but simple wins (front-line training, feedback loops) are achievable.

C. Institutional Brand

- Many smaller MFIs lack a trusted brand and are seen as temporary.

- Banks and cooperatives inspire more trust and long-term loyalty.

- Expanding services (savings, insurance, payments) can strengthen loyalty—if aligned with client needs.

D. Emotional Connection

- Personal bonds with loan officers are critical.

- Key drivers: advisory quality, punctuality, and transparent communication.

- Clients expect loan officers to support business growth—not just renew loans

E. Policy-Driven Attrition

- 12–15% of attrition is driven by MFI policies—not customer choice.

- Overly conservative renewal decisions tied to portfolio targets can unintentionally push out good clients.

- MFIs must refine attrition tracking to separate voluntary from policy-driven departures.

3️. Customer Profile & Needs

A. Diverse Needs

- Clients want business solutions—not credit for its own sake.

- They seek a suite of services: savings, insurance, training, and advice.

- Treating all clients as uniform credit-seekers leads to attrition.

B. Segmentation & Targeting

- Effective retention requires deeper segmentation:

- Demographics.

- Behavioral profiles

- Psychographic insight

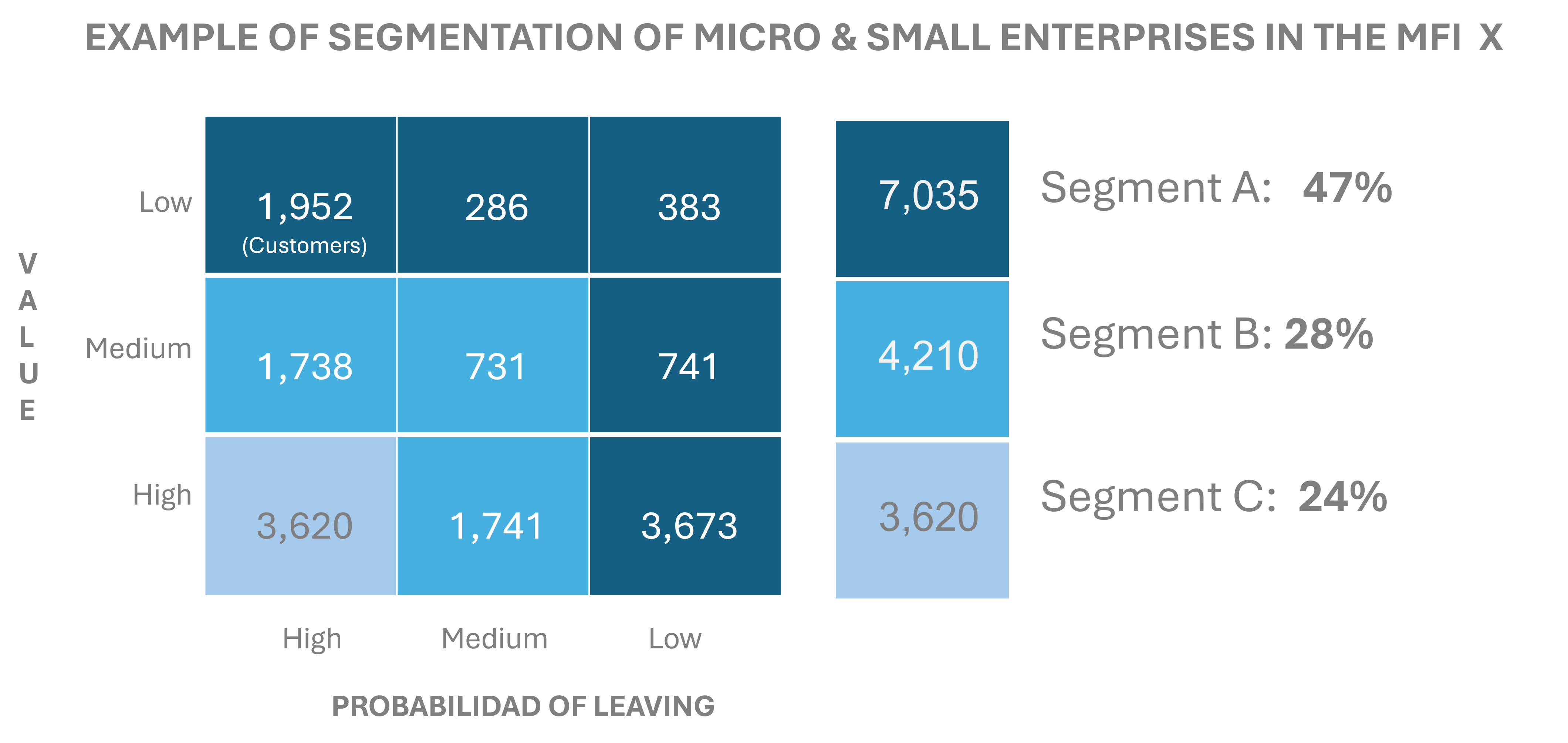

Predictive tools, such as desertion scorecards, can help MFIs proactively identify clients who are at risk of leaving. The matrix below illustrates how to segment customers based on both their likelihood of attrition and their overall value to the institution—enabling more targeted retention strategies.

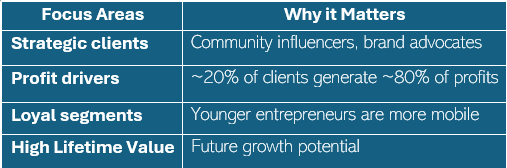

C. Prioritizing Retention Efforts

MFIs must be strategic—not all clients should be retained equally, some have more value than others

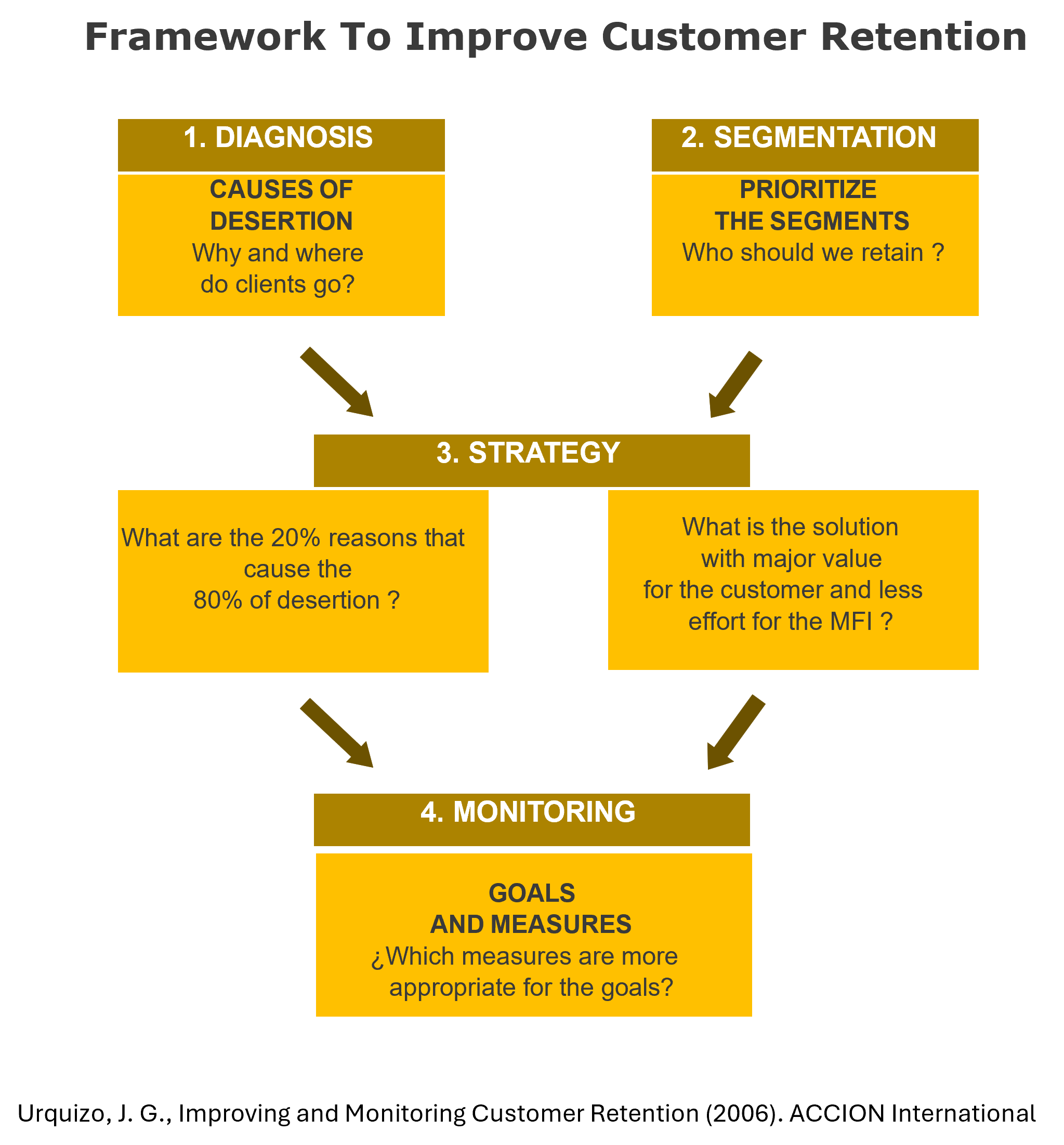

4️. Retention Strategies & Measurement

A. SystematicApproach

B. Managing “Resting” Clients

- Distinguish seasonally inactive clients from true deserters.

- Use behavioral segmentation to tailor re-engagement.

C. Tracking Retention

- Use a cause-effect model to identify the true drivers of attrition.

- Monitor multiple dimensions of customer retention; below are some indicators to help interpret the desertion rate or renewal index and track variables based on the causes of attrition.

D. Best Practices for Measurement

- Set clear goals.

- Focus on trends, not isolated points.

- Apply the Pareto principle (20/80 rule).

- Report absolute numbers and percentages.

- Align measurements with credit cycles.

- Allow one year before classifying as attrition.

- Use moving averages to smooth seasonality.

- Engage third-party researchers for objectivity.

Final Thoughts

By systematically applying these principles and improving measurement andsegmentation, MFIs can strengthen long-term client relationships, drive sustainability,and generate greater value—for both clients and institutions.

Source: Urquizo, J.G., Improving and Monitoring Customer Retention (2006). ACCION International.

https://www.findevgateway.org/paper/2006/01/improving-and-monitoring-customer-retention.