Designing Financial Services for a Market That Lives in Two Worlds

Immigrant consumers do not operate within a single economic or emotional system. Many earn income in the United States while supporting families,obligations, and long-term goals in another country. Their financial decisions are shaped by dual identities, cross-border responsibilities, and evolving aspirations.

In banking, immigrants, segmentation methods based on income or demographics alone fail to capture this reality. Time spent in the UnitedStates influences stability, familiarity, and confidence. Mindset shapes whether people see their future as temporary or rooted, which in turn affectsrisk tolerance, trust in institutions, and financial behavior.

This blog focuses on one of the most fascinating consumer segments in the United States: immigrants who live simultaneously, physically or mentally, in two worlds, the United States and their home country in Latin America.

The blog presents a market segmentation developed for a bank seeking to approach immigrant segments through cross-selling remittance services in the United States.

Understanding the Market: Immigrationas a Journey, not a Status

A critical insight in segmenting immigrant markets is recognizing thatbeing an immigrant is not a fixed condition, but a process. As immigrants spend more time in the United States, their priorities, risk tolerance, and relationship with institutions, especially financial ones, evolve.

Early stages are dominated by urgency and survival. Earning income,sending money home, and minimizing risk take priority. Over time, stability increases, families reunite, and future-oriented goals such as saving, investing, or building credit become more relevant.

This evolution means that the same person may move across segments overtime, making static segmentation models insufficient. Instead, segmentationmust reflect phases of integration and shifting worldviews.

Research into immigrant financial behavior shows that two variables are especially powerful in explaining differences across segments.

1. Time spent in the United States correlates with economic stability,familiarity with systems, and confidence.

2. Legal status and attitude toward thefuture, particularly whether individuals see their lives as temporarily or permanently rooted in the United States.

These drivers are far more predictive of behavior than income alone. They influence trust in formal institutions, risk management, and how money is allocated between countries.

Four Attitudinal Segments: BeyondDemographics

Using these drivers, the market can be segmentedinto four attitudinal profiles, each represented by a persona. While originally developed for financial services, these segments are broadly applicable to marketing, product design, and service delivery across sectors

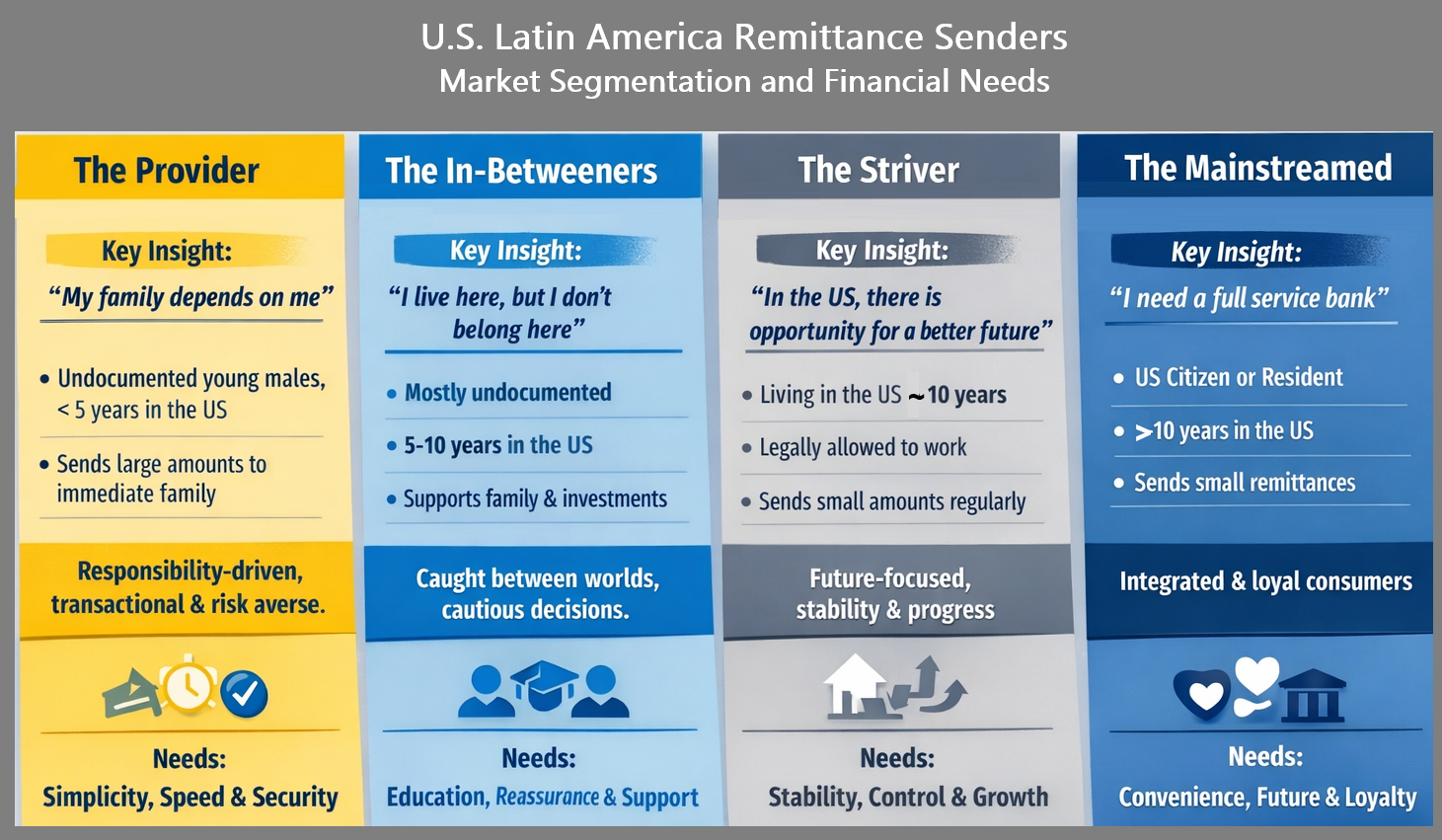

1. The Provider

Key insight: My family depends on me.

Profile: Undocumented young males with a strong sense of instability.They send larger amounts to immediate family for living expenses and debt repayment and have been in the United States for less than five years.

This segment is defined by responsibility. Financial behavior is transactional, habitual, and risk averse. Products that introduce friction, long-term commitments, or unfamiliar processes face strong resistance.

Design implication: Simplicity, speed, and trust signals matter more than features or long-term value propositions.

2. The In-Betweeners

Key insight: I live here, but I do not belong here.

Profile: Mostly undocumented individuals who send larger amounts to their immediate family for living expenses and investment. They have typically been in the United States for five to ten years.

This segment is caught between worlds. They feel neither fully rooted inthe United States nor fully connected to their country of origin. Their behavior is inconsistent, and their decision-making is cautious.

Design implication: Education, reassurance, and personal interaction arecritical. Digital-only or highly automated solutions may struggle without strong trust-building mechanisms.

3. The Striver

Key insight: In the United States, there is an opportunity for a betterfuture.

Profile: Individuals who send money semi-regularly in smaller amounts to support extended family back home. They have lived in the United States for more than ten years and are legally allowed to work.

This group represents a turning point. They have spent enough time in the United States to envision a future there, even if it still feels uncertain.Their financial needs begin to shift from pure transactions toward stability,control, and progress.

Design implication: This is often the most attractive segment for product development because they are open to new solutions, provided those solutions reduce fear and complexity.

4. The Mainstreamed

Key insight: I need a full-service bank.

Profile: Legal residents or United States citizens who have lived in thecountry for five to ten years. They send small amounts to support extended family back home. Socially integrated, this group behaves more like mainstream consumers, although emotional ties to their home country remain. They tend to already use formal financial products and services.

Design implication: Competing for this segment requires differentiation rather than access. Emotional and practical switching costs are high.

Why Attitudinal Segmentation WorksBetter

Attitudinal segmentation captures nuance and allows financial institutions to design for progression, supporting customers both in their current phase and as they move from one phase to another.

For example, two individuals with the same income may respond very differently to the same product depending on the phase they are currently in.

Trust is not built through branding alone, but through culturalfamiliarity, language, and perceived control.

Key Takeaways for Marketers andProduct Teams

This example demonstrates that when segmentation is done well, it becomesmore than a marketing exercise. It becomes a strategic lens for innovation and long-termimpact, as shown through applied market research on immigrant financialbehavior.