From Aspiration to Action: Advancing Inclusive Housing Finance Through Integrated Solutions

Housing in low-income markets serves a purpose beyond shelter. It can build household equity, generate income through rentals or home-based businesses, andact as collateral for credit. As such, housing finance is a critical pillar offinancial inclusion. Yet access to suitable housing finance remains a widespread challenge.

While many aspire to improve or expand their homes, financial, behavioral,and knowledge barriers often hinder progress. A practical solution combines tailored credit, savings, family collaboration, and technical support. Unlike traditional mortgages, low-income households typically pursue incremental housing improvement aligned with cash flow.

This blog distills lessons from diverse housing microfinance projects. Itoutlines demand`s drivers, evolving household needs, the role of financial institutions, and the impact of government incentives, while highlighting opportunities for collaboration to expand inclusive housing solutions.

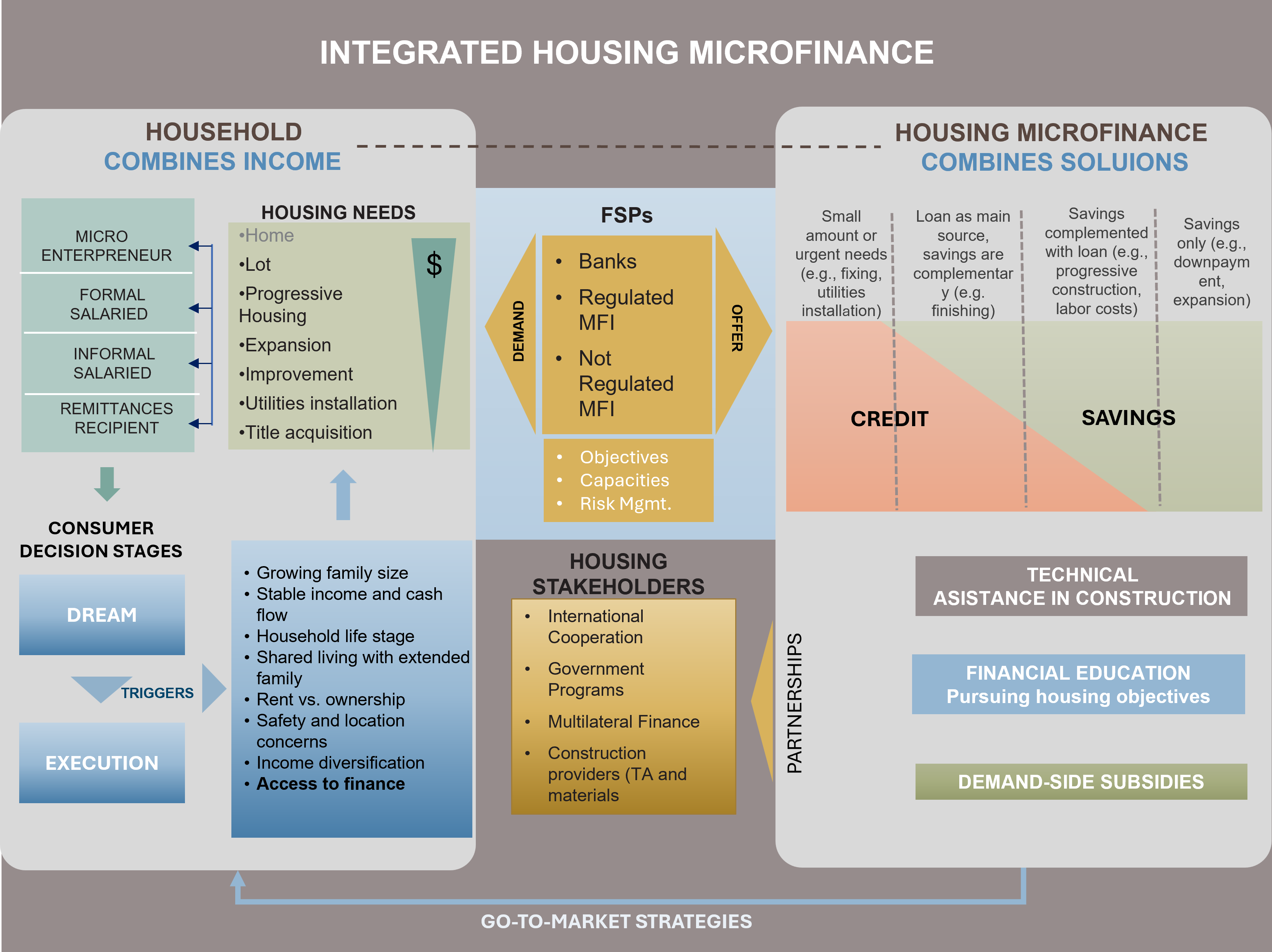

1. Market Demand and Consumers'Decision Dynamics

Behavioral Overview

Millions of families engage in aspirational housing projects, from basic upgrades to incremental builds. However, inertia sets in when urgent expenses(health, food, education) overshadow long-term goals. Elevating housing inbudget priorities is essential to housing demand creation.

Key Investment Triggers

- Stable income and cash flow

- Household life stage

- Growing family size

- Sharedliving with extended family

- Rent vs. ownership

- Safety and location concerns

- Income diversification (e.g., home rentals, small businesses)

Understanding these triggers enables tailored intervention to move households from "dream" to actual investment in housing purposes.

2. Household Needs and Investment Patterns

Land First: Securing land tenure is often the pre-requisite. Once acquired, incremental building aligns with irregular income and lowers financial risk.

Home Improvement: Demand centers on adding rooms, water, sanitation,and electricity. Few pursue full-home purchases; most opt for modular, phased upgrades.

Property Titles: Many lack legal ownership, limiting credit access.Financing title formalization is essential to unlock property value.

Financing property titling is essential to unlock housing value and improve equity leverage capacity.

3. Financial Offer Architecture

Housing finance differs from traditional MFI portfolios, which focus on short-term working capital. Housing loans are larger, longer-term, and often involve multiple household contributors. Emotional and technical dimensions require nuanced product design.

Product Formats:

- Credit-Only:For urgent, low-cost needs like repairs or basic utilities .

- Credit+ Savings: Loans form the core; savings close funding gaps.

- Savings+ Credit: Savings drive the project; credit complements specific costs.

- Long-TermSavings: Targeted at land purchase or down payments via disciplined savings

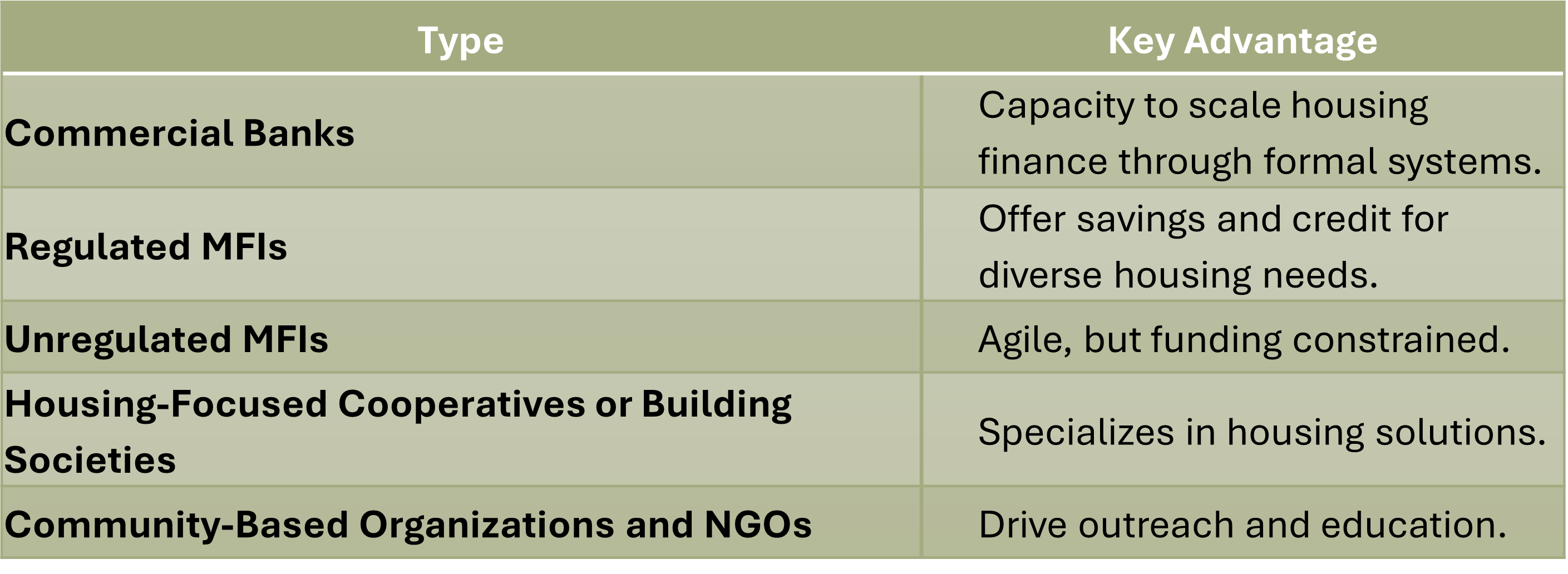

4. Institutional and Capability Requirements

Financial institutions aiming to enter the housing microfinance marketshould assess

- Strategic Fit: Product alignment with mission and client base.

- Risk Management: Tailored underwriting and repayment models.

- Market Execution: Effective channels, marketing, and outreach.

Various financial service providers (FSPs) and stakeholders can participate in this market,each bringing distinct capabilities and operational strengths.

5. Ecosystem Collaboration and Partnerships

- Governments:Shape policy, offer subsidies, and finance housing. Whether through demand-side subsidies (e.g., direct housing vouchers ) or supply-side interventions (e.g., public housing construction).

- Multilaterals:De-risk lending through guarantees and concessional funding.

- Technical Partners: Support construction quality (technical and materials).

Integrating Stakeholders

- Customer-Centric Products: Adapt to construction practices and income cycles.

- Construction Advisory: Offer training, vetted suppliers, and planning tools.

- FinancialLiteracy: Provide budgeting and credit guidance and behavioral change via NGO partnerships

Advantages for FSPsTargeting Housing in Emerging Economies

- Lenders:Gain portfolio diversity, larger ticket sizes, and access to new customer segments.

- Savings Institutions: Benefit from deposit stability and a pipeline building for credit products.

Partnershipsenhance outreach, reduce risk, and boost product uptake.

In a Nutshell

Housing microfinance represents a compelling business opportunity and a high-impact development intervention. Financial institutions that invest in understanding the demand triggers, craft integral offers, and engage instrategic partnerships can unleash the benefits of housing as a financial asset, supporting millions of underserved families while enhancing portfolio stability and deposit retention.

Acknowledgments: Special thanks to Mery Solares, whose on-the-ground insights were key to developing this comprehensive overview of housing microfinance.