Inclusive Savings: Design Lessons from Underserved Markets

Inclusive Savings: Design Lessons from Underserved Markets

While numerous studies explore how low-income households save, these insights remain confined to academic and research circles. This blog aims to bridge that gap by showing how consumer behavior can inform the design and execution of a marketing campaign.

Drawing from a case study of a small bank with 150 branches in Latin America in the early 2000s, we examine how savings behavior insights were applied to create an inclusive marketing campaign targeting the unbanked before banking agents became widespread. Although the campaign met its marketing goals, it also exposed critical gaps in a financial ecosystems that are still evolving.

This showcase includes the campaign's marketing strategy and ad brief,execution examples, and key lessons learned, many of which remain relevant today in underserved markets.

I. Marketing and Ad Brief

II. Execution

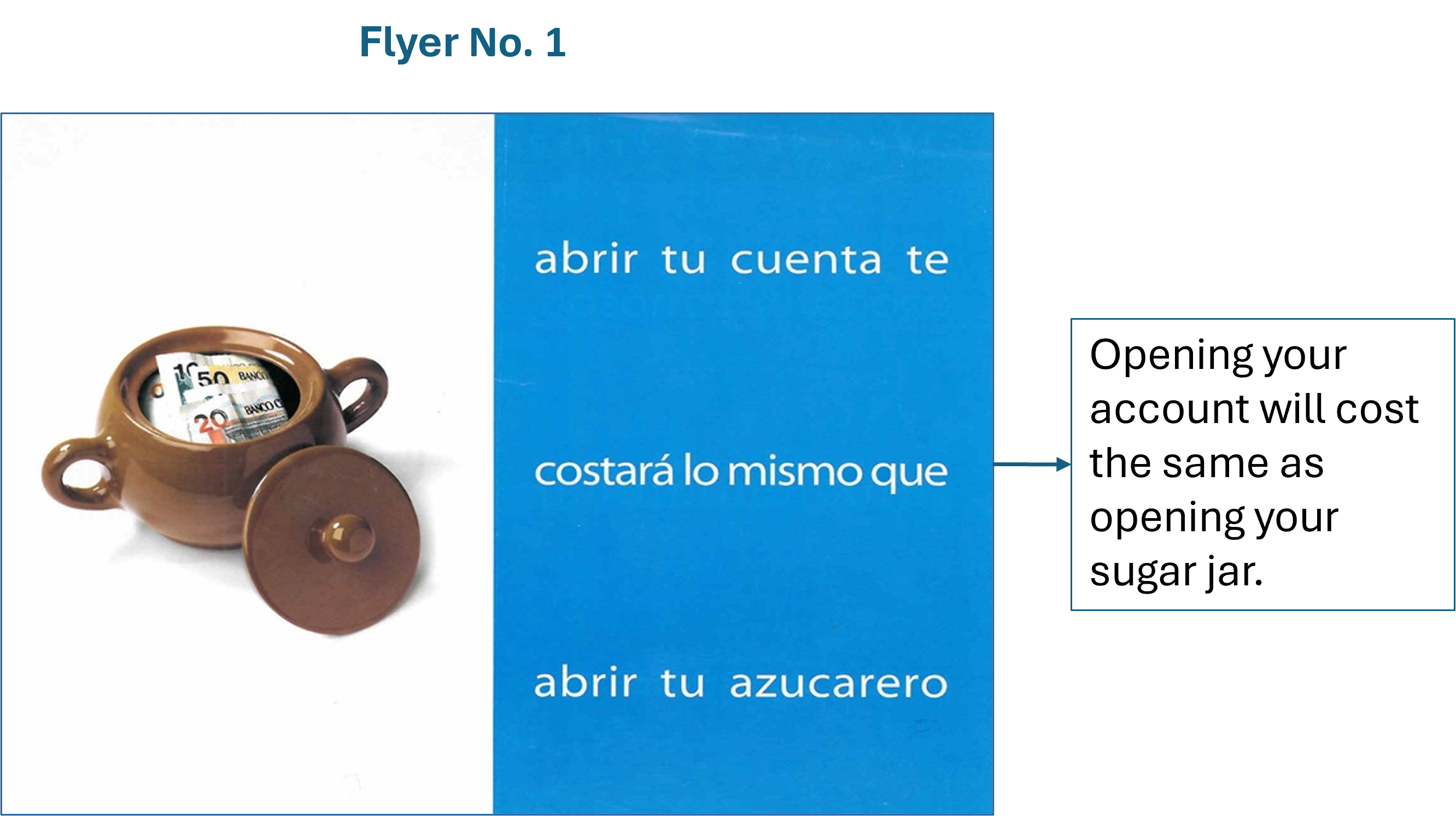

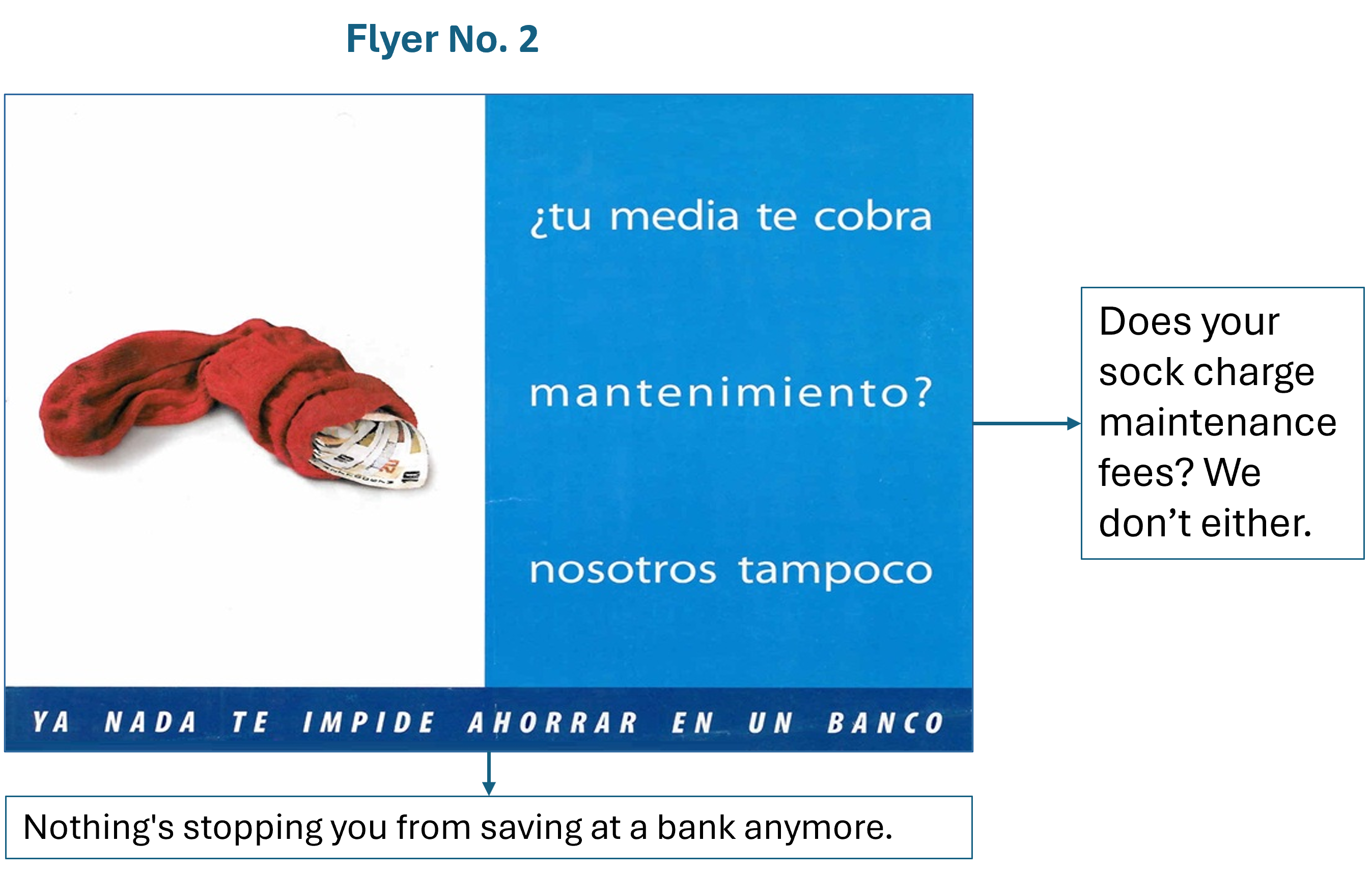

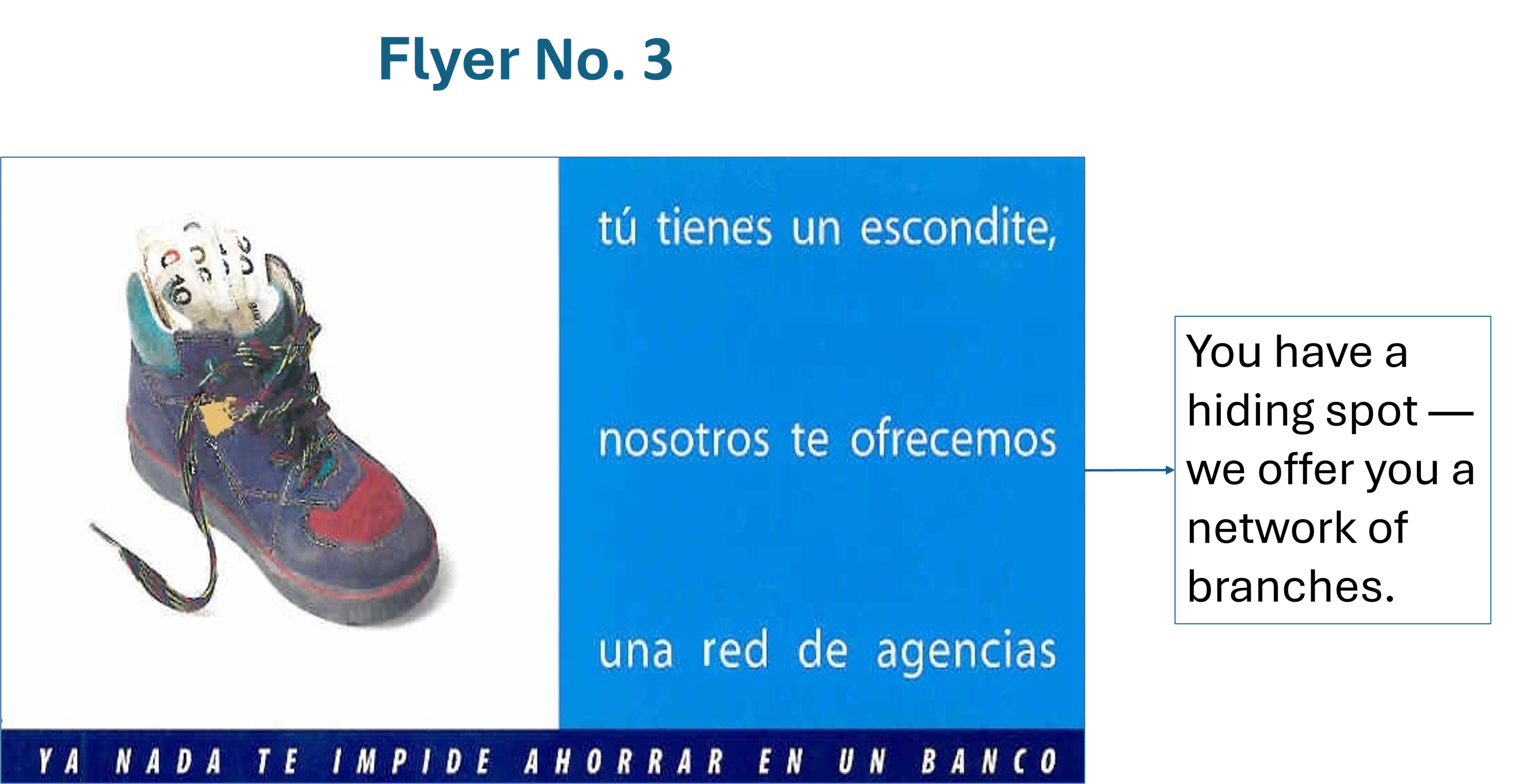

a) Press and Flyers

b) TV Commercials

SAFE PLACE TO SAVE

TOO SMALL FOR A BANK

III Main Takeaways for Banking the Unbanked Through Savings

While the campaign met its goals, itrevealed valuable lessons, many of which are now addressed by emergingtechnologies. These insights remain critical for designing effective strategies to reach unbanked populations:

- Coverage was Essential

Expanding geographic reach and offering multiple access channels proved to be the strongest driver of financial inclusion. Without accessible channels, there are no formal savings—even for non-transactional accounts. - What Unbanked Consumers Value Most

Immediate access to funds ranked highest among savings account features—above affordability, approachability, or interest earnings. - The Hidden Cost of Saving

Traveling to deposit money often costs more than the amount saved. Cost of saving was a primary factor in decision-making around formal accounts. Today, digital channels and digital money offer a scalable solution to this barrier. - Interoperability Extends Access

Interoperable systems across financialinstitutions and open finance would multiply reach and make formal savings moreaccessible.